Shortly after the opening bell on what ended up being the busiest session in U.S. stock-market history, an investor sold two shares of Amazon.com Inc. To a professor who analyzed that day’s trades, this tiny transaction illustrates a major flaw in the system.

The trade went through at $3,283.4901 per share -- one-hundredth of a cent better than what was officially the best available bid for the shares. That type of perk, however minuscule, is known as price improvement and is touted by market makers who match retail-brokerage buyers with sellers without using stock exchanges. Those fractions of a penny add up to billions of dollars a year.

Yet, at the same moment on the morning of Jan. 27, there was a bid available for Amazon on the Nasdaq that was actually $3.88 higher. That investor was only buying six shares, less than the 100-share increment that would qualify it as a “round lot.” Instead, it was a so-called odd-lot quote and therefore not included in the National Best Bid and Offer price benchmark that must be honored by all exchanges and trading platforms.

That transaction was far from the only one. Professor Robert Bartlett’s analysis found that more than a quarter of small trades in Amazon that day could have been done at more attractive prices for either buyers or sellers.

“You’ve got odd-lot prices that could be providing better prices and are sufficiently large to cover small orders,” said Bartlett, a securities-law expert at the University of California, Berkeley, whose study of that day was published last month. “The question is: Does it matter if you use a different benchmark?”

It does. And, given the surge in numbers of retail traders in the past year and their growing influence on the market, the debate over whether they actually are getting the best-possible prices is a hot topic in the industry now more than ever.

Regulators are trying to do something about it. The Securities and Exchange Commission last year announced a reform that would change the National Best Bid and Offer system by including orders of less than 100 shares for high-priced stocks like Amazon. Exchange operators sued to stop the plan, arguing it’s bad for markets and beyond the scope of the SEC’s authority. The changes have yet to be implemented.

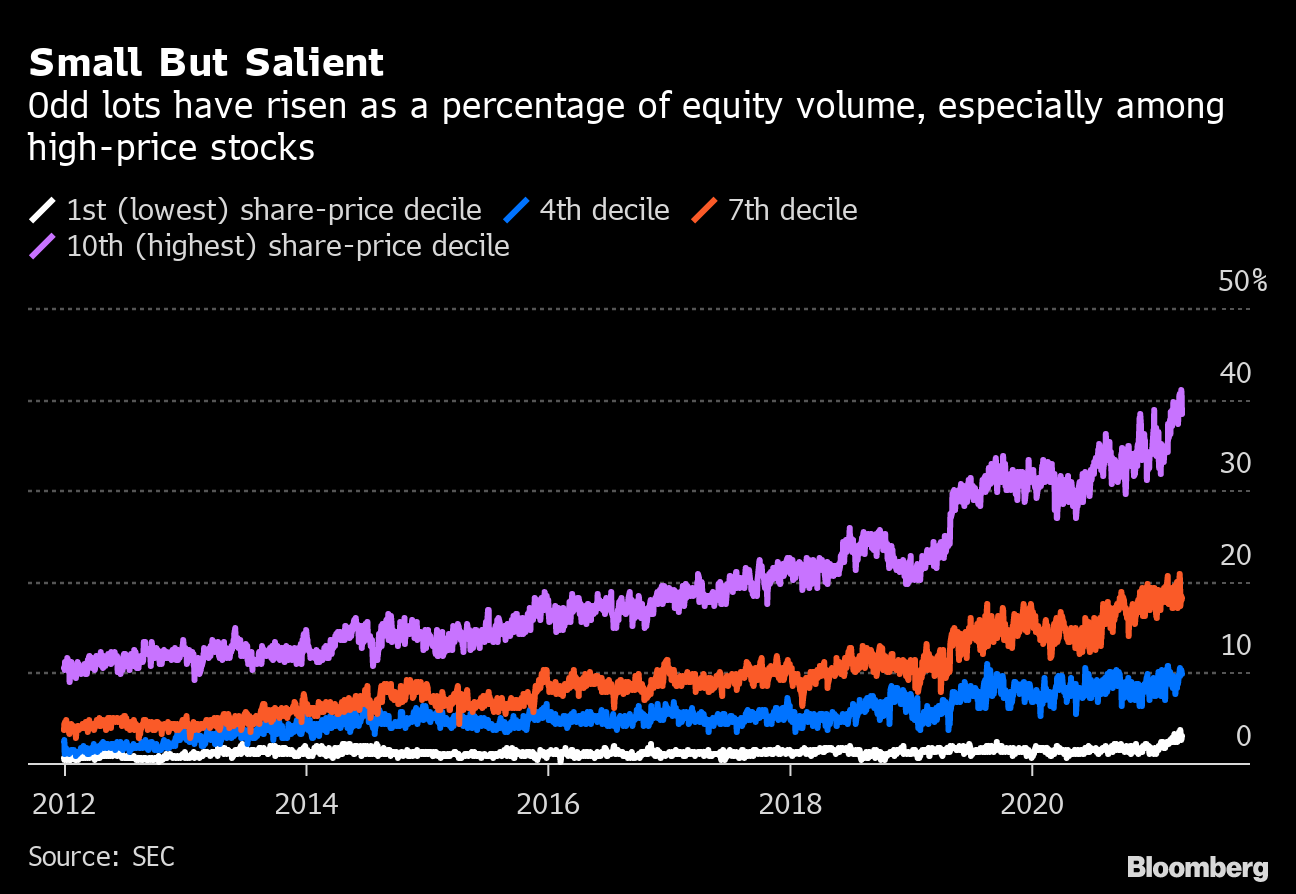

Small But Salient

Odd lots have risen as a percentage of equity volume, especially among high-price stocks

Source: SEC

The professor’s study of odd lots focused on the Jan. 27 session that marked the climax of the drama surrounding GameStop Corp. and other stocks favored by retail traders, a frenzied day that saw almost 24 billion listed shares change hands in the U.S. It turns out, Nasdaq also could have provided better prices that day for about 40% of odd-lot trades in GameStop that appeared to be retail orders executed by the electronic market makers known as internalizers, according to the study.

It’s a big claim, given the likes of Citadel Securities and Virtu Financial – who pay retail brokerages for their order flow – have long pointed at the price improvement they provide when defending their dominance of matching retail buyers with sellers. Bartlett’s findings – which echo other critiques of the status quo – suggest that these numbers are overblown relative to what traders could have received elsewhere.

To the internalizers, the problem is that the way retail execution is now evaluated doesn’t take order size into account. That means they aren’t getting credit for, say, giving price improvement on a larger buy order when the best quote from a seller is for fewer shares.

In its May policy recommendation, Citadel Securities said that incorporating such “size improvement” would outweigh any changes to execution statistics from including odd-lot quotes.

The required regulatory disclosure on execution quality, known as a Rule 605 report, “has three major weaknesses: it ignores odd-lot quotes, it ignores odd-lot orders, and it assumes infinite size at the NBBO,” Doug Cifu, chief executive officer at Virtu, said in an email. “Addressing these weaknesses in Rule 605 reports would help retail investors and the market to better understand the actual benefits received by retail investors.”

While small orders were once just minor nuisances relegated to specialized brokers in the floor-trading era, they have become increasingly commonplace and influential to the market. Odd lots rose from roughly 18% of reported trades in 2014 to half – and from 5% of volume to 20% by the end of last year. For high-priced stocks like Amazon, odd lots can make up nearly all daily trades, Bartlett’s research shows. Yet they don’t appear on the main data feeds accessible to the general trading public.

“Having odd lots not hit the tape gives investors a false sense of where the market is,” says Larry Tabb, head of market structure research at Bloomberg Intelligence. “When they get a price-improved trade, all they’re going to do is feel happy about the print because they didn’t know there was a better price out there. Is that a problem? Yes, but investors don’t really know.”

Bartlett argues his findings raise speculation that internalizers are ignoring sub-100-share order quotes despite having access to all available data. On the day he studied, there were 183,984 GameStop trades that could have been filled with sufficiently large odd-lot quotes. These orders enjoyed a total $123 of price improvement, but traders actually got worse prices than they likely would have if the smaller quotes had been included in the NBBO.

Source: Robert Bartlett. This example shows there are often better odd-lot quotes for high-price stocks like Amazon

To be clear, none of this disproves the price improvement offered by the internalizers overall, which totaled $1.16 billion last quarter across the six largest players, filings compiled by Bloomberg Intelligence show. Yet because the execution quality statistics internalizers are required to disclose only apply to round lots of 100-share blocks, little is known about the spreads on these smaller trades that make up the major chunk of retail orders.

There are reasons why internalizers can give Robinhood punters and other individual traders better spreads. Mostly it’s because their buying and selling poses less risk to these market makers than sophisticated traders like hedge funds who hold bigger positions and use computer algorithms to mask their intentions. For example, when an individual unloads a small number of shares, it’s usually not followed by further sales the way a pro’s trade might be. Neither is it likely based on any special insights. Internalizers, also known as wholesalers, can also execute trades in smaller tick sizes that are less then a penny, giving them more pricing flexibility.

Yet, Bartlett is not alone in his theory that they could do better. Alex Gerko, co-chief executive officer at XTX Markets -- a rival of Citadel Securities and Virtu -- says he observed a similar issue with retail trades earlier this year. His calculations show there was an additional $1.55 billion worth of price improvement versus the NBBO available last year simply with odd-lot quotes on exchanges. The shares most responsible for that were Tesla Inc., a high-priced stock beloved by the retail crowd.

“Retail PI statistics published by wholesalers are misleading,” Gerko wrote in a LinkedIn post, referring to price improvement.

In recent years, odd lots have faced much more scrutiny as share prices climbed and stock splits became less common – think Amazon, Alphabet and Berkshire Hathaway’s Class A shares, all famous stocks that trade above $1,000 a share.

To be fair, a market maker may avoid an odd-lot quote on an exchange because, while the price is attractive, it may be too small or likely to disappear in the fast-paced world of algo trading. That is traditionally why these quotes are excluded from the NBBO, the so-called protected quotes that ensure no trade anywhere can be executed at prices worse than the best ones at any given time.

“There might be good reason why they discount it,” said Bartlett, referring to odd-lot quotes. “But there’s also the possibility that my findings suggest that there are many non-exchange venues that are benchmarking off the price-protected NBBO even though the odd-lot orders could have filled the marketable orders.”

Still, Mark Davies, chief executive officer at trade analytics firm S3, says the market makers have a natural advantage in offering better prices.

If odd-lot quotes are incorporated into public feeds, “on certain given orders it may indicate a lower price improvement, but I don’t think it would likely change the overall aggregated numbers,” said Davies, whose firm helps brokers like Robinhood compile execution data.

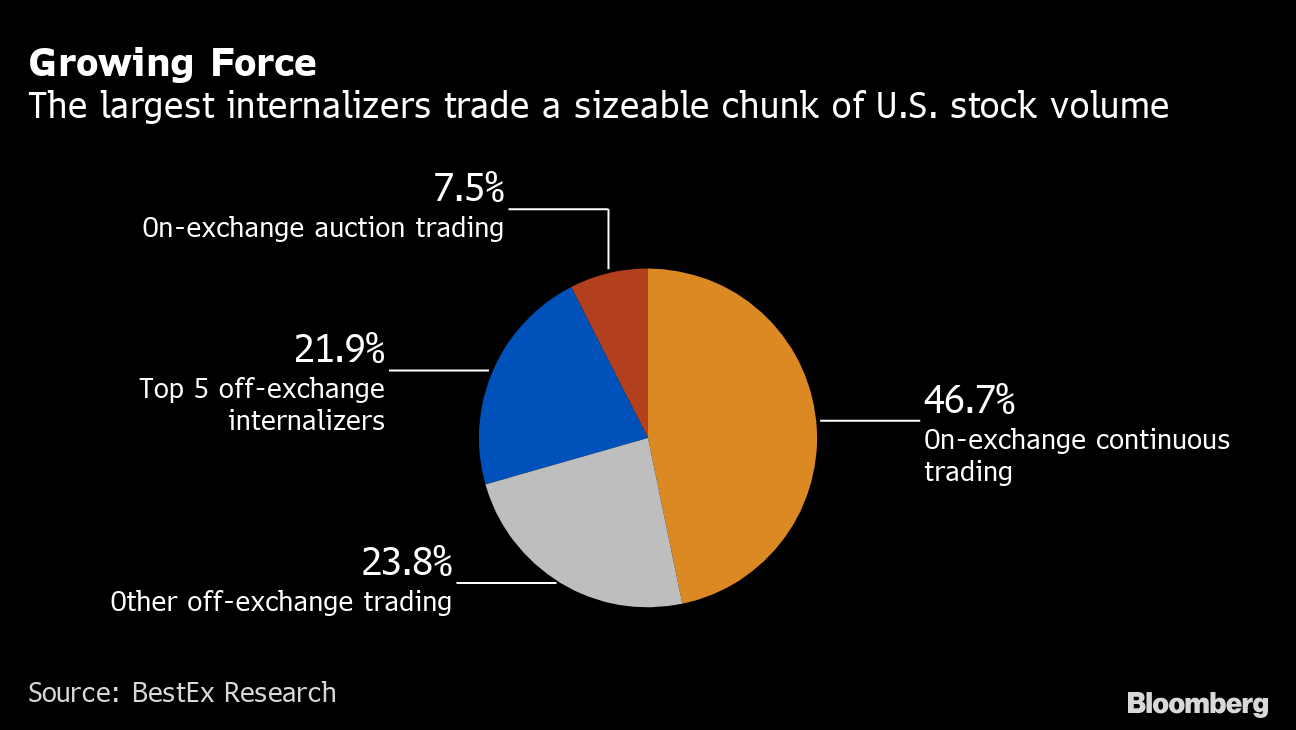

Growing Force

The largest internalizers trade a sizeable chunk of U.S. stock volume

Source: BestEx Research

Yet to critics, odd lots are one example of how internalizers consistently overstate their benefits to day traders and create distortions for the wider market.

Investors enjoy an average price improvement on exchanges that’s worth 8.7% of the bid-ask spread, compared with the 24.5% they receive from internalizers, according to a new study by BestEx Research, an algo shop founded by the former head of trading at quant giant AQR Capital Management. But if retail flows moved to exchanges and intermingled with institutional money, the NBBO spread itself would narrow 25%, making everyone better-off, the firm says.

That underscores how the growing role played by odd lots and internalizers has pushed significant chunks of volume into the darker corners of the market, where data is not available to all. Just 42% of trading in S&P 500 stocks last year could be seen by all market participants on exchanges, according to a Cowen Inc. study.

“As the percentage of displayed volume that is traded on-exchange declines, the quality of our market data degrades,” Jennifer Hadiaris, Cowen’s head of global market structure, wrote in the March report. “This has a real impact on all investors – retail and institutional alike – who rely on those displayed quotes to price and execute orders.”

The SEC reform would partly fix this. A round lot for a high-priced stock like Amazon would be 10 shares instead of 100, while stocks trading below $250 would still be considered odd lots in orders up to 99 shares. The best odd-lot quotes would also be included in the commonly available feed from the Securities Information Processor, which disseminates data throughout the market. Nasdaq, Cboe and the New York Stock Exchange –which stand to lose from having to make more data available cheaply – have sued the regulator to block the change.

NYSE has previously voiced support for adding odd-lot quotes to the tape and reforming the 100-share definition. Nasdaq has proposed a different solution that gets rid of the distinction altogether. Both declined to comment.

The SEC’s planned reform “sends a signal that these things are supposed to be incorporated when pricing non-exchange trades,” Bartlett said. “If they have the odd-lot quote in the core data, under what circumstances can they trade through them? That’s going to be the big question.”

"share" - Google News

June 09, 2021 at 05:00PM

https://ift.tt/3v90JS5

Two Amazon Shares Shine Spotlight on U.S. Market's Odd-Lots Flaw - Bloomberg

"share" - Google News

https://ift.tt/2VXQsKd

https://ift.tt/3d2Wjnc

Bagikan Berita Ini

0 Response to "Two Amazon Shares Shine Spotlight on U.S. Market's Odd-Lots Flaw - Bloomberg"

Post a Comment